You are standing on the frozen tarmac of a dealership just outside Mississauga. The wind cuts through your coat at minus ten Celsius, but you hardly notice. The air smells like wet pavement and cheap showroom espresso, mixing with the sharp scent of new tire rubber. You have spent weeks agonizing over trim levels, cargo space, and all-wheel-drive capabilities, finally settling on the exact Ford Explorer sitting gleaming in the weak November sun.

The sticker price looks perfect. It aligns precisely with the manufacturer’s suggested retail price you researched from your living room sofa. You walk through the heavy glass doors feeling prepared, armed with pre-approved financing rates and a firm mental boundary on your monthly payments. You are ready to sign the papers and drive your family home in a reliable, spacious new vehicle.

But the reality of modern car buying rarely happens out on the showroom floor. It happens in a tiny, artificially lit back office tucked away near the service bays. Here, the straightforward math you brought with you slowly evaporates, replaced by a subtle choreography of paper shuffling, digital signature pads, and vaguely reassuring corporate speak.

You are not buying metal and glass anymore. You are navigating a sophisticated financial ecosystem where the actual cost of your SUV is buried under layers of non-negotiable add-ons, masked as absolute necessities to survive Canadian winters.

The Illusion of the Final Number

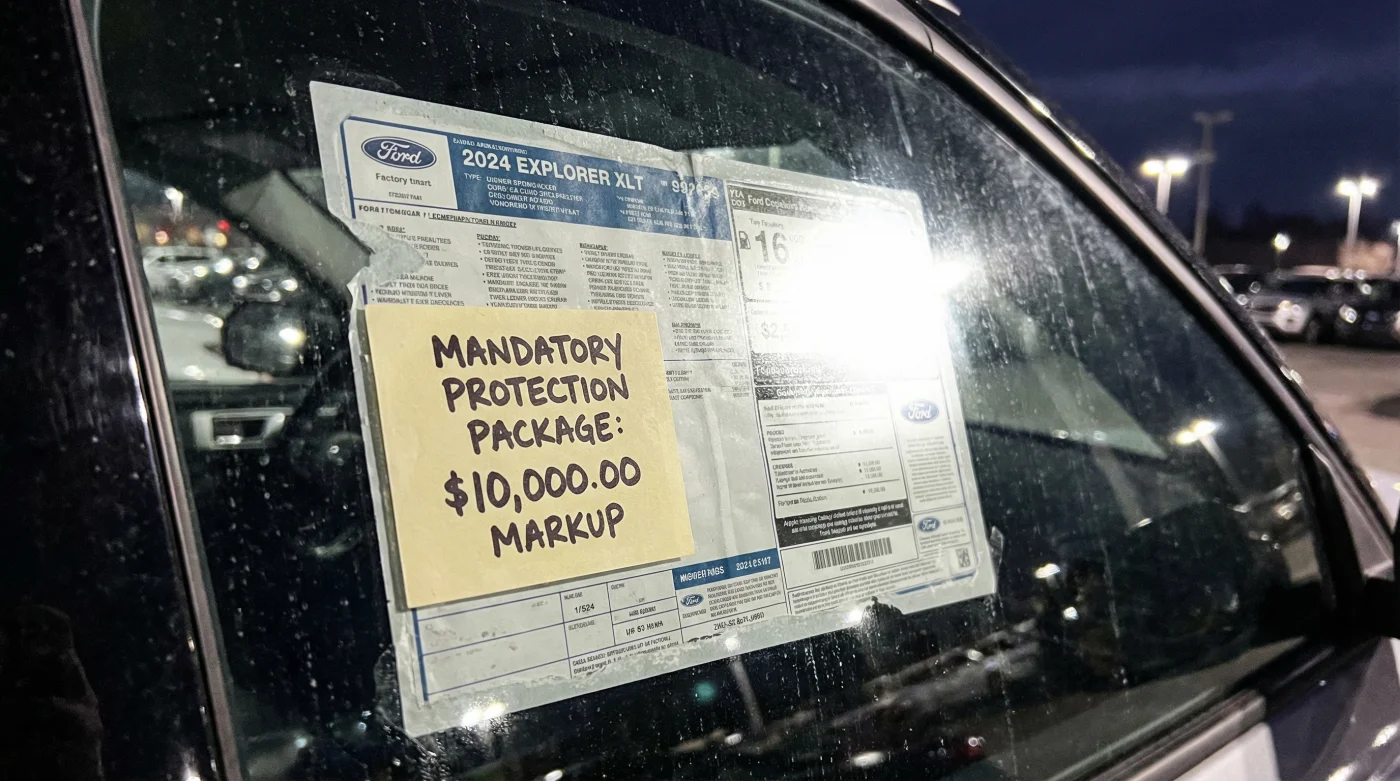

Think of the advertised price as a politely suggested starting point, rather than a binding contract. We have been conditioned to believe that negotiating a vehicle is a straightforward tug-of-war over the window sticker. The modern reality is closer to a sleight of hand performed by a highly trained illusionist. Dealerships have realized that slapping a blatant five-thousand-dollar markup on the dashboard alienates buyers immediately and drives them to the competition down the road.

Instead, they use financial camouflage. The massive markup has simply been rebranded for the modern era. You sit down with the finance manager, and suddenly, an exorbitant ceramic coating or interior fabric guard appears on the final contract. It is pitched as a local necessity to combat highway road salt, but in truth, it is a mandatory profit engine designed to bypass the factory pricing rules.

Marcus Vance, a 48-year-old former auto finance director in Calgary, calls this tactic the soft fortress. ‘They build a fortress around the actual profit margin using a driver’s fear of the elements,’ he explains. ‘I used to tell my team to refuse any financing deal unless the buyer accepted our proprietary paint sealant. We charged three thousand dollars for a chemical spray that cost us forty bucks in the service bay. It was never about protecting the clear coat against the Alberta snow; it was about protecting the dealership’s bottom line against a highly competitive digital market.’

The Anatomy of the Buyer Profile

The finance office does not use a one-size-fits-all approach to bury these mandatory protection fees. They read your priorities during the test drive and tailor the trap to match your specific buying style. Understanding your own profile is the first step to dismantling their strategy before the ink dries.

For the Payment-Focused Parent: You care deeply about the monthly number because you have a household budget to maintain. The finance manager recognizes this and stretches your loan term from sixty to eighty-four months, quietly folding the three-thousand-dollar protection package into the principal. You barely notice the bump because the monthly figure looks manageable, even though you will pay thousands in extra interest over the next seven years.

For the Cash Buyer: You think you are completely immune to financing tricks because you are bringing a certified cheque to the table. The dealership counters your leverage by refusing the sale outright unless the dealer-installed accessories are paid for in full. They frame it as a strict company policy—a pre-applied chemical treatment they simply cannot wash off the chassis, forcing you to pay for a product you never wanted.

- Honda Odyssey chassis rigidity secretly underperforms against standard Kia Sedona frames.

- Used Subaru Outback roof rails reveal critical structural rollover damage instantly.

- Routine brake fluid flushes secretly introduce microscopic moisture into ABS modules.

- Lexus RX base models utilize thicker acoustic glass than luxury editions.

- Ford Explorer dealership markups hide mandatory paint protection fees in financing.

Dismantling the Finance Trap

Protecting yourself from these forced markups requires a complete shift in your posture at the dealership. You must stop treating the finance manager as a helpful administrative clerk and recognize them as the final, most potent salesperson in the building. Their entire job is to sell the financing paper, not the vehicle.

Patience is your absolute shield. When the final contract slides across the heavy wooden desk laden with unrequested line items, do not argue about the chemical quality of the paint product. Simply refuse the premise of the charge altogether. Strip the emotion out of the room.

Follow a sequence of mindful, minimalist actions to strip the contract back to reality:

- Request the official buyer’s order before discussing any financing terms, interest rates, or monthly payment structures.

- Ask for a line-by-line itemization of the out-the-door price in writing, explicitly separating the vehicle cost from accessories.

- State clearly that you will not pay for any dealer-installed accessories or protection plans that you did not explicitly request.

- Be prepared to walk out the front doors, no matter how much emotional energy you have already invested in this specific vehicle.

Maintain a strict tactical toolkit. Target your threshold by refusing any mandatory fee exceeding one hundred and fifty dollars for standard administrative licensing. Use a definitive key phrase: ‘I will take delivery today at the agreed retail price, but I firmly decline all pre-installed protection packages.’ Give the finance office exactly fifteen minutes to redraw the paperwork without the artificial fluff, or politely end the transaction.

Reclaiming Your Purchase Power

Stripping away these hidden fees is about far more than just saving a few thousand dollars on a new Ford Explorer. It is about establishing a firm boundary in an environment historically designed to wear down your patience and separate you from your money. When you learn to spot the artificial padding buried in the paperwork, you fundamentally change the power dynamic of the entire automotive transaction.

You drive away with clarity. Instead of feeling that familiar, lingering knot of buyer’s remorse, wondering if you were quietly taken advantage of in the final hour, you feel a profound sense of ownership. Your vehicle becomes a true symbol of your financial autonomy, rather than a heavy steel monument to a local dealership’s profit margin. The open road ahead feels a little lighter when you know exactly what you paid for.

‘The moment you stop treating the finance office as a formality, you reclaim the power to dictate the true cost of your vehicle.’ – Marcus Vance, Automotive Finance Veteran

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| The Hidden Markup | Paint protection fees disguised as mandatory local necessities. | Prevents you from overpaying thousands for low-value add-ons. |

| The Term Stretch | Hiding total package costs by extending the loan up to 84 months. | Helps you focus on the principal balance rather than the monthly illusion. |

| The Walk-Away Power | Setting a 15-minute deadline for the dealer to remove forced fees. | Gives you an actionable boundary to stop high-pressure sales tactics. |

Frequently Asked Questions

Are dealership paint protection plans actually mandatory?

No. Despite what a finance manager might tell you, forced accessories are a dealership policy, not a legal or manufacturer requirement. You have the right to refuse them.What if they say the coating is already applied to the vehicle?

You politely inform them that you did not request the application and will not pay for unauthorized modifications to the vehicle’s factory state.Can they refuse to sell me the Ford Explorer if I decline the fees?

Yes, an independent dealership can refuse a sale. However, signaling your willingness to walk away often forces them to drop the fees to save the transaction.Why do they hide the markup in the financing office?

Because buyers fiercely negotiate the window sticker price. Burying profit in the finance paperwork catches exhausted buyers off guard at the end of the process.Is third-party paint protection a better option?

Absolutely. Independent detailing shops offer superior ceramic coatings at a fraction of the cost, applied with specialized care rather than a quick spray in a dealer service bay.