The showroom smells faintly of industrial floor cleaner and stale roasted coffee. Rain lashes against the vast glass panels, blurring the neat rows of vehicles parked outside in the brisk five degrees Celsius Canadian chill. You are gripping a glossy brochure for the new Subaru Crosstrek, staring at a printed number that feels perfectly aligned with your carefully calculated budget.

You anticipate a straightforward transaction, a simple exchange of signatures for keys. Yet, the reality of modern car buying operates on a completely different frequency, one where the advertised price is a suggestion rather than a binding contract.

You sit down in the finance manager’s office, the air suddenly feeling heavier. A piece of paper slides across the desk, and the number at the bottom no longer matches the one in your hand. The gap between those two figures is where the real business of selling cars happens.

Most buyers assume consumer protection laws prevent sudden price hikes at the desk. However, a clever restructuring of dealership preparation fees legally bypasses strict Canadian MSRP advertising limits, shifting the financial burden back onto you through forced services.

The Phantom Tollbooth of Auto Finance

Think of the advertised MSRP as the entrance to a long, winding toll road. The manufacturer sets a strict ceiling on what they can advertise, a law designed to protect you from bait-and-switch tactics. But the dealership controls the tollbooths positioned along the final stretch of pavement between the lot and your driveway. You might plan to drive a hundred miles out of the city this weekend, but first, you have to pay the gatekeeper.

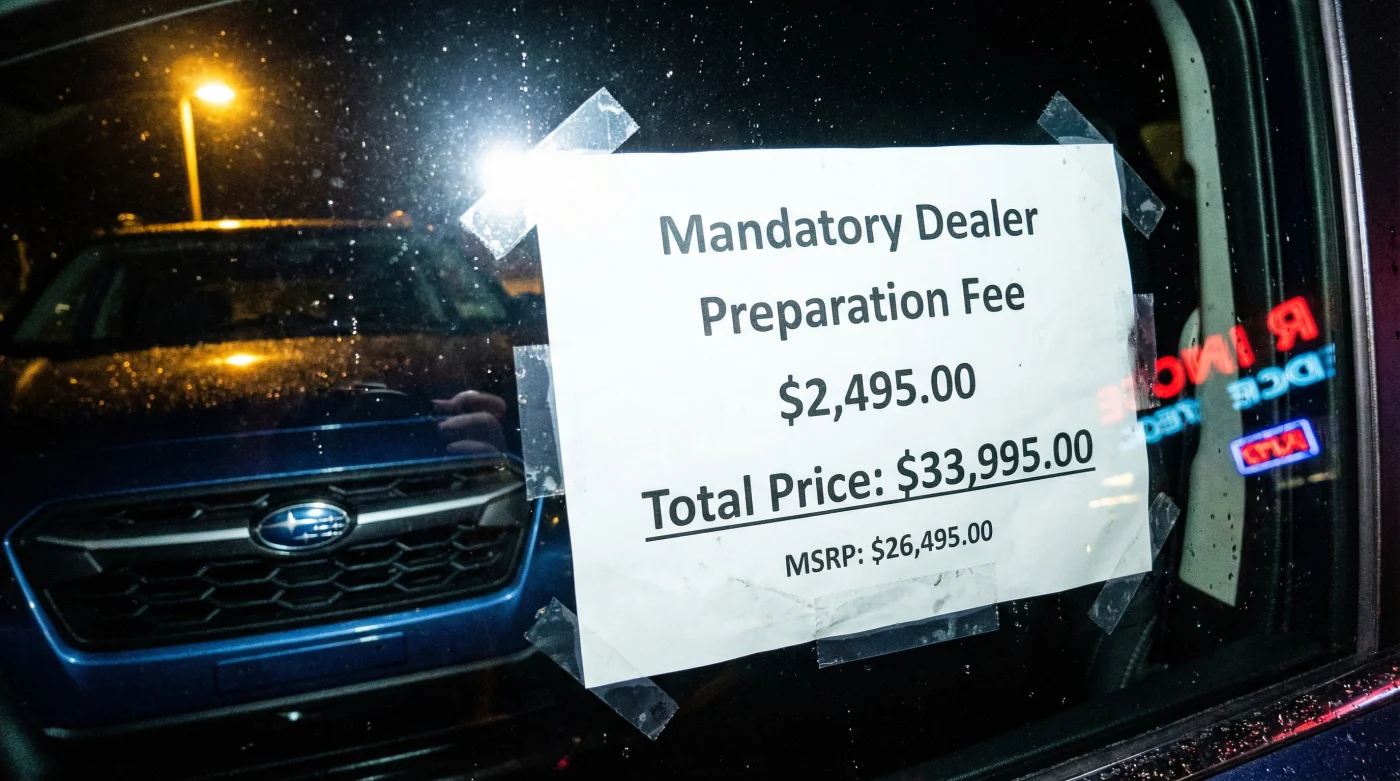

They call them mandatory preparation fees, administration charges, or security etching costs. These line items act as a financial sponge absorbing the margin that dealerships are otherwise forbidden to add directly to the base sticker price. It is a brilliant, albeit frustrating, pivot from charging more for the car to charging more for the privilege of buying the car.

Marcus, a forty-five-year-old former dealership finance director operating out of Burnaby, spent a decade writing these exact contracts. “We couldn’t touch the MSRP without facing massive fines from the regulators,” Marcus explains, leaning over a faded coffee cup. “So, we baked our profits into the prep phase. We’d charge hundreds for a mandatory cabin sanitization or a localized rust module. If a customer pointed to the all-in pricing law, we’d smile and say the law only covers the car itself, not the mandatory local services required to release it from our specific lot.”

His admission reveals a profound truth about the modern automotive market that most consumers never realize until it is too late. The vehicle itself is no longer the primary product; the paperwork is the profit centre.

Segmenting the Impact: Who Pays What?

Not all buyers interact with these hidden fees in the same way. The dealership adapts its approach depending on how you intend to pay for your Crosstrek, subtly shifting the narrative to make the prep fees feel like an unavoidable tax based on your profile.

- Acura MDX aluminum suspension components fracture faster than basic Honda Pilot steel.

- Jeep Wrangler carpet removal reveals hidden dangerous offroad chassis torque warping.

- Toyota 4Runner factory transmission fluids accelerate premature planetary gear wear significantly.

- Ford Bronco base models utilize stronger solid steel differential mounting brackets.

- Subaru Crosstrek dealership prep fees bypass legal Canadian MSRP advertising limits.

For the Leasing Loyalist: The fees are often quietly baked into the capitalized cost of the lease, stretching a nine-hundred-dollar prep fee across forty-eight months of payments. It feels like pennies a day, camouflaging the reality that you are paying interest on an administrative loophole.

For the First-Time Financer: The finance office will frame these preparation fees as a prerequisite for swift loan approval. They bundle the vehicle preparation with mandatory gap insurance or warranties, making it exceedingly difficult to untangle the actual cost of the metal from the cost of the financing requirements.

Mindful Application: Defusing the Contract

Regaining control requires a deliberate, almost minimalist approach to the conversation. You must strip away the emotion and treat the contract like a puzzle that needs careful disassembly. Breathe through the tension, ignore the ticking clock, and focus entirely on the line items.

Do not argue about the total final number printed at the bottom of the page. Instead, force the finance manager to justify every individual line item before you even pick up a pen.

- The 24-Hour Hold: Never sign on the same day you receive the final worksheet. Take the paperwork home, sit at your kitchen table, and calculate the actual cost of the added fees.

- The Red Pen Method: Physically cross out anything labelled “Prep,” “Admin,” or “Etch.” Hand it back and politely ask them to print a clean sheet without the lot fees.

- The Factory Call: If they insist a fee is required, offer to call Subaru Canada directly from the showroom to verify if a “mandatory regional rust treatment” is a true factory requirement or a dealer add-on.

- The Walk-Away Point: Decide on a hard ceiling before you enter the dealership. If the mandatory prep fees push the price a single dollar over that line, stand up and walk toward the exit.

Beyond the Final Number

Pushing back against these fees is not merely about keeping a few hundred dollars in your bank account. It is about establishing firm boundaries in a system designed to wear down your resolve. When you understand the mechanics of the pricing structure, the dealership loses its power of intimidation.

When you successfully strip away a phantom fee, you drive off the lot with something far more valuable than a pristine new vehicle. You leave with the quiet satisfaction of retaining control over your own money.

“A contract is just an opening offer written in formal ink; the true price of any vehicle is decided in the silence after you say no.” – Marcus, Automotive Finance Veteran

| Key Point | Detail | Added Value for the Reader |

|---|---|---|

| MSRP Limits | Canadian law restricts advertising above the manufacturer’s set price. | Provides the legal baseline you need to challenge sudden price jumps. |

| Prep Fee Loophole | Dealers mandate lot-specific services to bypass the advertising ceiling. | Identifies exactly where the dealer hides their pure profit margins. |

| Itemized Auditing | Striking out ‘Admin’ and ‘Etching’ fees before signing. | Equips you with a physical tactic to reduce the out-the-door cost. |

Frequently Asked Questions

Are dealership prep fees actually mandatory in Canada?

No. While dealers present them as mandatory for their specific lot, they are entirely negotiable and not required by the manufacturer.Does the all-in pricing law protect me from these charges?

The law mandates that the advertised price must include all fees, but dealers bypass this by claiming the prep fees are separate, optional services that you are forced to accept.What is the best way to refuse an admin fee?

Ask them to show you the manufacturer mandate for the fee. When they cannot, request a clean contract without the charge.Will a dealer refuse to sell me the Crosstrek if I won’t pay the prep fee?

In high-demand markets, they might threaten to, but most will concede the fee rather than lose a guaranteed sale sitting right in front of them.Should I negotiate the out-the-door price or the monthly payment?

Always negotiate the out-the-door price. Focusing on the monthly payment allows the finance office to hide prep fees by simply extending the term of your loan.